Published

Can China Make up for the West?

By: Fredrik Erixon Oscar Guinea Vanika Sharma Renata Zilli

Subjects: Far-East Russia & Eurasia

The Russian economy is in disarray. The Russian ruble is in free fall; sales of foreign exchange are banned; and foreign companies are fleeing Russia day by day. In a previous blog we showed the high level of economic interdependence between Russia and the rest of the world, particularly with the EU which accounts for more than one third of Russian exports and imports. A lot has been said about Europe’s dependency on Russian oil and gas, and this dependency remains an acute problem. However, in macro terms, the Russian economy is much more dependent on the EU than vice versa.

Financial and economic sanctions have made trading with Russia a risky proposition. These sanctions include the removal of Russian banks from the SWIFT system and restrictions to access key foreign currencies, making it hard for Russian banks to get loans, process payments and use foreign exchange. Western companies have been banned from selling certain goods to Russia, including oil refining equipment and technology, aircrafts, spare parts, and equipment, dual-use goods and technology equipment, semiconductors, and computers. The sanctions also include an explicit prohibition of doing business with a number of Russian state-owned companies.

The financial and reputational risks for doing business with Russia are so high that many companies have stopped operating in Russia. And even if companies want to sell their goods to Russia, they might not be able to supply them since Maersk, MSC, FedEx, and UPS have stopped their shipments to Russia. Moreover, receiving payment for these sales has also become more difficult as Visa and Mastercard no longer work in Russia. Many companies leaving Russia have headquarters in countries imposing these sanctions – like South Korea’s Samsung and Taiwan’s TSMC – which explains their departure from the Russian economy, but many others, including Chinese companies and multilateral institutions, have followed the same exit path because doing business in Russia has become too complicated. As Russia finds itself in more economic trouble, Russian policymakers could resort to policies reserved for a command economy including expropriation or the requirement to buy from specific suppliers.

Yet, as the financial and trade sanctions isolate Russia from the global economy, a question hangs over EU and US policymakers: can China make up for the West?

We attempt to shed some light into this question using trade data. However, our analysis suffers from some limitations. First, we compare the monetary value of EU and US exports to Russia with the monetary value of exports from other major global exports from countries that have not imposed sanctions on Russia. These monetary values do not necessarily reflect the quantity or the quality of the traded products. Even if the monetary value of a country’s total exports could make up for the monetary value of EU and US exports to Russia, we don’t know if the quantity or quality of these goods is sufficient to substitute EU and US exports to Russia. Second, the trade statistics used in this blog are the most detailed available but despite working with thousands of trade codes, they are product categories not individual products. The same product category would cover an entire shelf in a supermarket, with a huge variety in product quality and functionalities. This means that exports of the same product code from different countries include different individual products, and the comparison of one country’s exports with another is far from perfect. Third, the substitution of one country’s exports for the same product made by another company is not easy and that is not captured in the trade statistics, particularly with regards to manufacturing goods and complex products which constitute the bulk of Russian imports. Issues around standards and compatibility, licencing and property rights, and the fact that modern production of any product is embedded into a supply chain which include final products, parts, components, tools, and machines needed to produce other manufacturing goods, make the substitution of goods between countries far from easy, particularly in the short-term.

We start with a list of more than 1,500 products for which Russia is largely dependent on EU and US firms. Then we turned to the global exporters of these products with the exceptions of those countries imposing sanctions on Russia. China is the largest exporter of the products in which Russia relies mostly on EU and US companies, accounting for 1,059 of all product categories, followed by India with 101, Thailand with 63, and Turkey with 63. For the majority of these trade categories the value of these countries’ exports exceeds the value of EU and US exports to Russia, but not always. This is not surprising. China is the largest exporter of goods in the world; and the Russian economy is not particularly large ranking 11th in global GDP tables. Still, there were 34 product categories – including machine tools, engines, medicines, and medical devices – for which EU and US exports to Russia were larger than Chinese total exports.

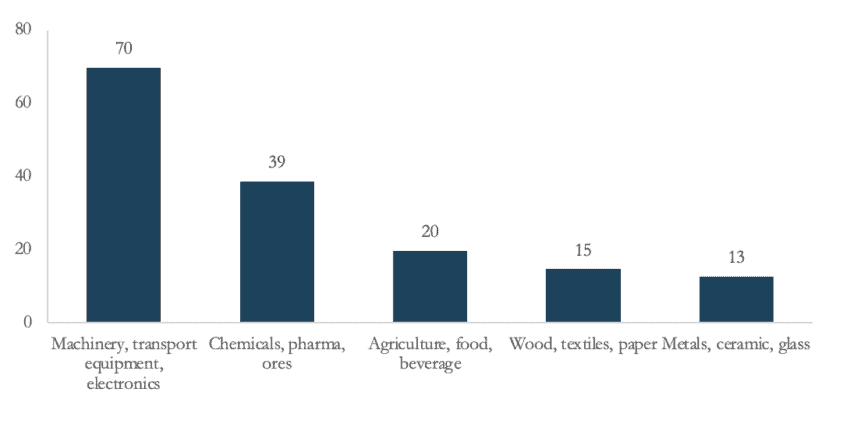

A ratio of 1 to 1 is a high bar to meet. Chinese exporters cannot ditch previous business commitments on a whim to sell their products to Russia. In our analysis, there were 157 product categories for which EU and US exports to Russia were at least one third of Chinese total exports. As shown in Figure 1, these products belong to the machinery, transport equipment, electronic, chemical, and pharmaceutical sector. However, the value of these exports is small, accounting for just 2 percent of Russian total imports. Yet, shortages of some products could permeate multiple economic sectors, in particular when these products are difficult to source somewhere else, are key inputs in the production of manufactured goods, or vital goods for citizen’s well-being like medicines.

Figure 1: Number of product categories in which EU and the US exports to Russia were at least one third of Chinese total exports

Source: UNCOMTRADE, authors’ calculations.

The fact that EU and US products can be substituted by Chinese exports does not mean that they will be substituted, particularly with the Russian economy in turmoil. The question, then, is not whether Chinese businesses can substitute EU and US companies, which in the long-term they can, the question is if Chinese companies will fill the void now when the Russian economy is in great distress.

China’s deeper integration with Russia offers opportunities: a market to sell Chinese manufacturing goods and from which to buy energy, but this choice is not risk-free. Chinese exports to Russia increased by 18 percent between 2017 and 2020 but Russia remains just the 14th most important market for Chinese goods, representing just 2 percent of Chinese total exports, far from the importance the EU (15%) or the US (17%) hold as a foreign market for Chinese businesses. The bottom line: it is not in China’s interest to overthrow the world economic order because it benefits enormously from it. Despite all the talk about dual-circulation, China’s economic model remains outward oriented. Between 2019 and 2020, Chinese exports grew by 4 percent, while EU and US exports fell by 7 percent and 13 percent respectively. Moreover, China is not in a position to offer an alternative to the US dollars. More than 40 percent of global payments are settled in dollars, while the renminbi accounts for 2 percent. There is no doubt that the Chinese currency will grow in importance – particularly in Russia – but it cannot compete with the US dollar yet. Russia’s decision to invade Ukraine has united the West and triggered a spike in energy and agricultural commodities prices – many of which China is a large importer of. The risk for China is to be left isolated from the West as the talks about strategic autonomy, technological sovereignty, and dependencies are followed by a common EU and US approach to these challenges, leading to both nations working together to offset the distortive effects of Chinese non-market policies on the global economy.

At the firm level, there are individual business opportunities for Chinese companies to supply goods to Russia, but the current economic uncertainty and risks may be too high for Chinese companies to step into Russia right now. The volatility of the Russian ruble will make it difficult for Chinese companies to sell their products in Russia without incurring losses or charging a much higher price tag to compensate for these fluctuations, which may be hard to afford for Russian customers at this moment. And the sanctions throw additional risks for corporations, as Chinese companies need to weigh the drawbacks of possible violations of Western sanctions and the reputational risk of being associated with Putin’s war on Ukraine.

In return Russia offers cheap raw materials to China. This is not necessarily out of goodwill. Dependency is a two-way street and Russia is desperate to find new buyers for its exports, particularly now that the EU is actively planning to lower its gas purchase from Russia and the US has banned Russian oil. The EU and the US are key markets for Russia exports: in more than 600 product categories, the EU and the US account for more than half of Russian exports. These exports represent 15 percent of Russian total exports and include mostly oil and gas. China could buy some of these goods, but they represent a significant amount of Chinese current imports, and require an infrastructure that needs to be built. The EU imports twice as much oil and gas from Russia than China and EU imports of some of these products from Russia represent a significant proportion of Chinese total imports. The data shows that Russia cannot easily divert its main exports to China as it’ll face constraints in terms of pipeline capacity and Chinese refining capacity.

And why would China want to become dependent on Russia’s raw materials? China is witnessing how western nations are suffering because of their dependency on Russian oil and gas. China is a large importer of energy, but it will not make itself vulnerable to the extent that Russia can use energy exports as a political tool. Despite the Sino-Russian Agreement signed in February 2022, there is a history of mutual distrust between Russia and China, which includes historical territorial grievance between the two nations that share a border of more than 4,000 kilometres and competing interest in Central Asia.

The Chinese economy has the capacity to fill the void left by the EU and the US, but this will not happen overnight. Uncoupling the Russian economy from the West will be costly – and these costs have been heightened by Russia’s war on Ukraine – and will take a long time as many of EU and US exports to Russia are part of larger technological systems for which it is not possible to change components quickly. Businesses make decisions based on their own self-interest and even though the Russian market offers opportunities for Chinese companies, they might not be ready to walk the plank and, instead, they might want to sit on the fence until the Russian economy stabilises. Meanwhile, Russian production capacity will continue to be hammered by the effect of sanctions.

A thoughtful reply. Of course, there are some non-economic factors, such as saving face, that will also be at play.